Tax Break for Small Business Owners Making $400K - $600K

By: Patrick Cote

If you are a small business owner making $400K - $600K, there is a large potential tax savings that you have likely not heard about. It involves combining the new 20% QBI deduction with a cash balance/defined benefit plan.

Many people do not know that they can bring down their taxable income by up to ~$250K by setting up 401K plans combined with a defined benefit or cash balance plan. This is very important for folks who miss the 20% QBI deduction, because contributing to these retirement plans can mean getting an extra $64K deduction!

For owners of an S corporation or LLC, you may have heard about the 20% QBI (qualified business income) deduction that was rolled out last year. This deduction is available whether the standard deduction is taken or deductions are itemized. Engineers, architects and real estate agents do not have a limit on their income to get this 20% QBI deduction, however other businesses that are based on reputation/skill face a limit. Most other businesses have a phase-out that kicks in with taxable income of $321,400 (married filing jointly) or $160,700 (single), which means the 20% QBI deduction is fully phased out at $421,400 (married filing jointly) or $210,700 (single).

If your taxable income is above the threshold limits, you may have been told that you make too much money to get the QBI deduction. That is, of course, a great problem to have! However, setting up the combined 401K and cash balance/defined benefit plans can bring down your taxable income enough to qualify for the QBI deduction, which translates into significant tax savings.

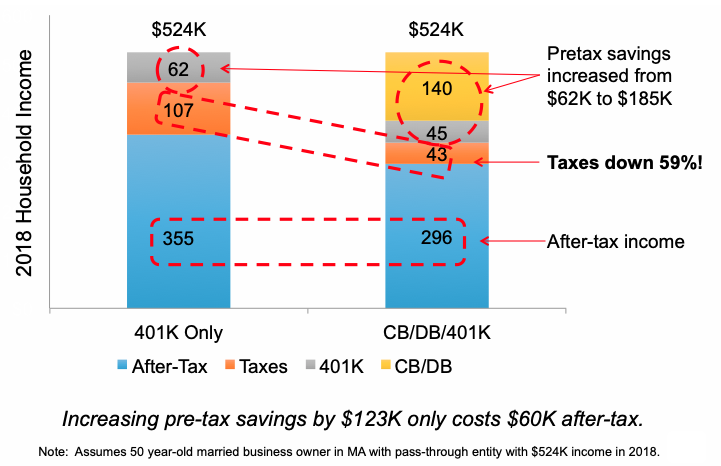

An example shows just how dramatic the savings can be. For a 50 year-old married business owner with $524K in taxable income last year, if they contributed the maximum of $62K to their 401K, they would have after-tax income of $355K.

By saving $140K in a cash balance plan, coupled with $45K in a 401K, they would have increased their pretax savings from $62K to $185K. The amazing aspect is that their after-tax income only fell by $60K. In other words, they were able to increase their pre-tax savings by $123K and it only cost them $60K after-tax!

If you are wondering why you have not heard about this, it is because not many CPAs and investment advisors are able to help with cash balance or defined benefit plans. Specialized retirement plan and actuarial expertise is required, which means that most of the large brokerage firms are not able to offer this to their clients.

Because the tax savings are so significant, if this situation applies to you, it is worth the effort to find an investment advisor that can help!